$TH 3Q'24 Update

Recent Developments Create Lottery Ticket Opportunity

For context, TH 0.00%↑ is a workforce housing provider in Southwest Texas with a market cap of ~$850mm which has shifted its operations towards government operations. I first posted my thoughts on TH 0.00%↑ about a month ago on Twitter (@DCap8252729) and I thought I’d post an update. This was originally supposed to be an update solely for my portfolio and I wasn’t planning on publishing this, but I figured the few who follow TH 0.00%↑ might be able to give their opinions.

Developments:

TH posted a resilient quarter as, despite the cancellation of its Dilley contract in June, the government segment fell only -10%. As residual revenue from Dilley dwindles, government segment revenue will likely normalize around its fixed rate of ~$45mm quarterly (=~180M contract/4). The firm’s HFS segment remained similarly consistent, posting quarterly rev of $38mm; over the past 8 quarters, this segment has had a standard deviation of $1mm, proving its stability due to LT contracts. TH’s cash balance also remains elevated at $178M, yet remains inline with LT debt which matures in the following 2 quarters.

Mgmt guided toward FY’24 revenue midpoint of $380mm, implying 4Q’24 revenue of $77mm, down -20% QoQ. This decrease primarily incorporates expectations surrounding decreased government segment revenues. TH also announced the anticipated extension of its PCC contract yesterday, despite occupancy of zero; the government further proves its desire to maintain ICFs on standby.

Importantly, TH is seeking to reappropriate its ~2.5K beds from the Dilley center towards government initiatives, yet mgmt has mentioned lethargic government communication, pointing to administration transition as justification.

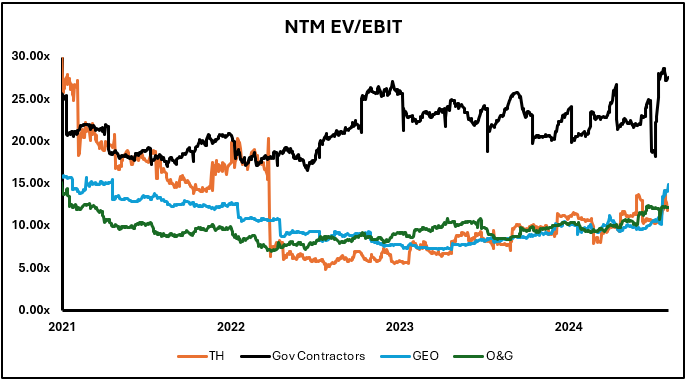

TDR’s retraction of its buyout offer in September resulted in a -25% share price fall, as TH’s NTM EV/EBIT fell -3x while its NTM P/E fell -3.3x to 13.4x. Since, Both its EV/EBIT and P/E rebounded to 14.3x and 24.8x last week, before tumbling back to 11.8x and 20.2x, respectively. The stock rallied post-election as a Trump administration seems to promise increasing immigrant apprehensions, yet the -15% tumble since Thursday seems to be a mixture of sentiment correction and Oppenheimer’s downgraded reinitiation with a price target of $9; I admittedly don’t place much weight on Oppenheimer’s forecast as their analyst doesn’t seem to follow TH too closely (rarely shows up on earning calls, associates ask simple questions, dropped coverage for a time, etc). Worth mentioning that Oppenheimer’s reinitiation was likely sparked by increasing interest, which seems appropriate given the multiple’s appreciation.

Upside:

1. Dilley/New ICF:

a. TH’s ~2.5K beds on standby at Dilley provide spare capacity which could be translated into revenue with little additional overhead. The old Dilley contract was priced at ~$60M with each bed contributing ~$23K of yearly rev, 25% of PCC’s rate. According to mgmt, the government remains consistent in their desire for new ICFs, yet the pricing will likely be at a lower rate than the PCC as the contract was signed during unexpected and unprecedented immigration inflow in FY’21. While an ICF demands greater expertise than a detention facility, which Dilley used to be, I deem it fair to assign any new ICF contract a price of 50% of PCC, or ~$45K yearly per bed. This would result in a Dilley contract of $115M. For context, the Greensboro ICF was awarded at $62.5K rev per bed in FY’22. The second new ICF contract was awarded to Greensboro in March, yet hurricanes sidetracked its opening, and the center was recently repurposed by the Federal Emergency Management Agency (FEMA) for training and processing. The repurposing of Greensboro leaves a contract up for grabs. It is important to note that this rate will only materialize if Dilley becomes an ICF, I believe it more likely that the facility will be reappropriated towards another government function, providing revenues similar to the old Dilley contract

2. Immigration:

a. If immigration apprehensions were to boom under the new Trump administration, variable revenues could prove game-changing and would provide tremendous upside. Taking a view on immigration is outside of my expertise and has little downside risk, so I refrain from fully forecasting. For now, this point should be viewed as optionality.

Downside:

1. Loss of Contract:

a. The PCC contract remains year-to-year, and its closure could provide downside of -35% (assuming the beds are repurposed at a lower rate as part of the HFS segment), yet both the governments words and actions (expansion of ICFs) point towards the very slim likelihood of PCC closure. The government extended the PCC contract this morning for another year, yet TH’s extreme customer concentration (56% rev from government) is a cause of concern.

2. Multiple Depreciation:

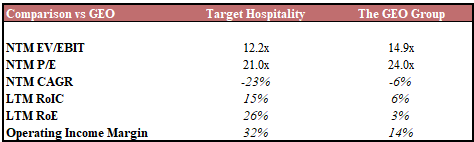

a. TH’s recent strength has been purely driven by a rerating by investors, likely as a result of both reversion to the mean and anticipation of favorable Trump policies. The stock had stabilized at 10x EV/EBIT (in line with O&G firms) before TDR’s buyout offer and Dilley’s closure, and further regression towards 10x would result in downside of -15%. TH’s closest comp, GEO, has maintained a EV/EBITs of 14.1x, despite a more commoditized service (Jails vs Turnkey ICFs), similar growth, and inferior margins (3yr EBIT margin of 15% vs TH’s 37%) and returns (3yr ROIC of 6.5% vs TH’s 23.8%).

Thesis:

At this point, any investment into TH would be due to its asymmetric bear/bull of roughly 1:3-5; I believe the downside case to be roughly -15% if the firm fails to find a suitor for the Dilley facility and if the multiple falls back to 10x, in line with O&G. Once again, I don’t believe the closure of the PCC to be a significant risk as the government’s word and actions seem committed to retaining ICF’s on standby, regardless of occupancy. Bull case is largely reliant on:

1. ICF contract win (+35% to EBIT, if new contract is 50% cheaper than PCC) which would likely push TH’s multiple closer to other government contractors (I believe this case would conservatively allow for upside of +50%

2. Variable revenue from immigration, which could provide upside of >100% due to revenue requiring extremely little additional investment.

I do hold shares in TH, but this name is primarily an asymmetric lottery-ticket type of investment, not an idea in which I have tremendous conviction.