$NCNO Initial Memo

Financial SaaS compounder, yet at a heavy price

Overview: nCino (“NCNO”) is the leader in cloud-based banking applications, offering a comprehensive suite of products to financial institutions ranging from local credit unions to multinational conglomerates. While NCNO’s stock has lingered at ~$30 per share since 2022, valuation remains expensive (~7x LTM revenue). I believe that NCNO’s superior platform, established switching costs, and economies of scale will allow the firm to maintain a +20% compounded earnings growth rate for multiple years, yet valuation remains expensive, and the main question revolved around their ability to maintain this growth above the market’s implied ~6-year time horizon.

History & Strategy: NCNO was originally founded in 2011 as an in-house cloud banking platform within Live Oak Bank (a small business lending bank headquartered in North Carolina), yet, as the value of the platform became obvious, the product and its team were spun out as a majority-controlled subsidiary. By 2014, NCNO began selling its first commercial lending units, bolstered by a $10M series A capital infusion from Wellington. As Live Oak Bank sought to divest in 2015, growth equity investors Insight Partners led a $29M series B funding round, later being joined by T Rowe Price and Salesforce Ventures, which provided momentum to both add product offerings while expanding into international markets. By NCNO’s Jul’20 IPO, the firm was valued at $2.8B (~9x EV/Sales), yet investors’ excitement quickly fueled an IPO pop to ~$8B. Since, NCNO’s shares have fallen -60%, yet the company has steadily continued to grow both its customer base and product size through tuck-in M&A. Additionally, management has explicitly emphasized its “land-and-expand” strategy, forecasting ~60% of future incremental sales stemming from cross-sells to existing customers.

Business Description: NCNO offers comprehensive SaaS solutions to financial institutions (“FI”), segmenting revenue into subscriptions (~85%) and professional services (~15%).

Subscription revenues are generated through contracts with FIs and host an average duration of 3.8 years. While NCNO initially focused on small, commercial lending institutions, the firm has sought to expand into consumer lending and mortgage (combined ~50% of revenues in FY’24 and has moved upstream to larger customers (Bank of America, Barclays, and Santander UK, to name a few). Subscription revenues can be further disaggregated into the Bank Operating System (estimated ~80% of subscription revenues), an end-to-end mortgage suite (confirmed ~15% of subscription revenues), and portfolio analytics (estimated ~5% of subscription revenues). Professional services entail system installation and support, which is usually outsourced to local tech consultants (“system integrators”) for large customers and is typically sold at-cost to small FIs.

Bank OS: An umbrella term which encompasses the bulk of NCNO’s operations and consists of a cloud-based platform designed to streamline operations for FIs. Bank OS products are listed below:

1. Enterprise Client Onboarding: Automated onboarding whereby clients quickly upload their own documents which are subsequently organized, verified, stored for regulatory purposes, and complemented with government and third-party data.

2. Deposit Account Opening: Similar to Enterprise onboarding yet tailored for deposit accounts. Information is similarly collected, verified, and compared to credit issuer data.

3. Loan Origination: Automated workflow and document management, allowing all stakeholders to have visibility in the process while providing FI employees with real-time insight into loan performance.

4. Automated Spreading: Provides a comprehensive view of FI’s client’s financial data and history, allowing for efficient credit analysis and loan underwriting.

5. Pricing & Profitability: Automated and intelligent analysis of loan profitability. Delivers real-time insights from the middle and back office surrounding price policies and recommendations.

While these capabilities are often performed by in-house solutions or siloed competitors, NCNO’s ability to consolidate into one platform allows for greater data management and administrative efficiency, seamless interaction within bank verticals, simplified regulatory compliance, and price savings through bundled products. As of 3Q’25 (most recent quarter as NCNO is on FY’25 until February 1st), over half of Bank OS customers use more than one product, a >15% increase since FY’22, with an estimated 30-40% using mortgage and portfolio analytic solutions as well. Moreover, NCNO hosts net revenue retention rate of ~120%, evidencing high switching costs. Notably, NCNO has been transitioning its pricing model from seat based to asset-on-platform based, allowing for variable revenues above a certain minimum commitment. Between FY’22 and FY’24, Bank OS customers grew from 394 to 460.

Mortgage: NCNO has been offering an end-to-end mortgage suite since its acquisition of SimpleNexus in 2022 (~$1.3B acquisition price, ~20x EV/Rev) which includes Loan-Origination-System and Point-of-Sale offerings. Similarly to Bank OS, the Mortgage segment automates document compilation, loan application servicing, verification, and insights to streamline the lending process. Since acquisition, mortgage sales have grown at a 14% CAGR despite ~15% churn in FY’24 as many Independent Mortgage Banks either consolidated or went bankrupt. Mortgage contracts are also priced on a consumption-above-minimum basis, and depressed home sales have hindered demand. Customers have grown from 428 to 434 between FY’22-24, peaking at 475 in FY’23.

Portfolio Analytics: Formerly Visible Equity, acquired in 2019 for $75M. Provides insight into a credit portfolio’s profitability, risk, and performance while ensuring compliance with regulation. The product is relatively commoditized and low-priced. Customers have grown from 1.1K to 1.4K between FY’22-24.

As of FY’24, 19% of NCNO’s revenues are outside of the US yet the firm has had recent contract wins in India, Japan, and Europe. International expansion has been a recent focus and also follows a “land-and-expand strategy” as few banks risk being the first to onboard a new platform, yet once one competitor does, many others seek to emulate. Initial penetration has thus far mostly been accomplished through M&A, international branches of existing customers, or connections through system integrators.

NCNO’s products are built entirely on Salesforce’s CRM and the firms re-inked an authorized reseller contract in Dec’23, which is set to run until 2031, allowing NCNO to install the CRM themselves to smaller customers; naturally, despite Salesforce’s easy integration, installation comes at a cost which could hinder growth amongst poorly capitalized smaller FIs.

Importantly, the firm has incorporated AI and ML into its offerings through nIQ, which executes and enhances its automated spreading, pricing & profitability, and portfolio analytics solutions. Additionally, NCNO recently released its Banking Advisor software; since few banks’ lending operations reach critical mass required for AI analysis, management hopes to leverage its large quantities of data to improve its analytical solutions.

Why NCNO Wins: NCNO competes directly with both in-house solutions and solution-specific competitors, yet no firm has been able to match its breadth of products. In-house solutions are often vestiges of legacy systems, frequently perpetuating inefficiencies as the FI scales; NCNO’s purpose-built offerings, strong marketing, and connections with system integrators and Salesforce allow for the initial contract within a firm, and as other legacy systems within the firm require updating, NCNO’s solutions become the clear choice due to aforementioned data management and administrative efficiency, seamless interaction, and price savings through bundled products. Moreover, interviews with anonymous customers routinely point towards NCNO’s platform’s flexibility and collaboration with Salesforce as key purchase factors. While stealing share from solution-specific siloed competitors is more difficult as NCNO’s technological superiority is nullified, the benefits of a one-platform offering remain, especially as these competitors often lack the flexibility to scale with the firm’s changing needs.

Management:

- CEO Pierre Naude: Has been CEO since the firm’s inception, before which he served as the divisional president of S1, a banking software platform. After a stint in the military, he worked his way through college in his thirties, receiving a BS in Finance and Management from Upper Iowa University in 1996. His compensation has shown little growth since FY’22, earning ~$500K base and $7.3mm bonus compensation in FY’24; he also holds ~0.5% of NCNO’s float. He is currently 66 years old, and has failed to definitively shut down retirement rumors when asked.

- C-Suite: NCNO’s C-Suite has experienced significant turnover in the past few years. Firstly, the former CFO was seemingly laid off in Jan’23, which coincided with broad expense cutting and a shift towards profitability. Additionally, both the CRO and CPO left in FY’24 on amicable terms, and their responsibilities have been absorbed by other executives. The current CFO’s compensation structure is similar to the CEO’s, yet he has received a ~40% bump since FY’22.

- Board of Directors: The board has eight members including the CEO and is permeated by both FI operations specialists and a panoply of investors (a credit investor, a venture capitalist, a private equity investor, and an investment banker).

Market Perception: NCNO has struggled in recent years, with little price appreciation since 2022. While investors were initially excited about a high-growth SaaS story, many became disillusioned by NCNOs slower moving nature, and the valuation pull-forward post-IPO has hindered NCNO’s appreciation. Moreover, high interest rates have placed downward pressure on variable consumption-based revenues while new customer wins have slowed as FIs operate gingerly during economic slowdowns. Yet, the market still believes in NCNO’s ability to grow, evidenced by nearly unanimous sell-side forecasted ~15% revenue CAGRs until ~2030 and a NTM revenue multiple of 6.3x.

Key Questions:

1. How long can NCNO maintain mid-high teens revenue growth?

Management has guided LT topline growth of ~15% as, despite having a very large TAM runway, financial institutions move very slowly due to both regulatory and cultural constraints. While NCNO’s 2yr rev CAGR of ~13% was hindered by a lethargic economy and likely understates its growth algorithm, yet growth significantly greater than 15% yearly remains unlikely. Granted, I do believe that strong retention rates and low penetration will allow NCNO to maintain these growth rates for far longer than five years.

2. Where will LT margins stabilize?

Management has ambitiously guided to a “Rule of 50,” implying operating margins to hover ~35%. NCNO’s LTM operating margin currently stand at -0.9%, yet for a software business low capital requirements and proven economies of scale, 35% seems achievable. In the past 4 years, both COGS and SG&A have decreased from 46% and 49% to 40% and 37% percent of revenue, respectively; COGS is likely to continue its decrease as professional services become a smaller portion of sales, and the emphasis on cross-selling will likely allow for decreased marketing expenses. My hunch is that 35% remains ambitious as R&D ( ~24% of revenues) will remain stickier than forecasted due to the constant need for integration and innovation of new capabilities, but a 30% LT operating margin seems within the range of possibilities.

Risks:

- Consolidation of Competitors:

Consolidation would nullify NCNO’s single-platform advantage, eliminating value-creation. Creating a platform with NCNO’s scale would take many years and customers would face high switching costs, but if successful, growth would slow substantially.

- Regulation:

The financial services industry is heavily regulated, strict legislation would both slow the rate of innovation and limit variable portion of revenues.

- Expensive M&A:

NCNO has performed numerous tuck-in acquisitions since founding, sometimes at very high multiples (i.e. SimpleNexus for 20x rev). Wasteful capital allocation could nullify the value of the firm’s cash flows.

Outlook: NCNO is best-of-breed in an under-penetrated industry and has proven its strength through numerous high-profile contracts. Moreover, the industry’s slow-moving nature and steep learning curve forced NCNO to spend ~10 years establishing its comprehensive product and high integration switching costs provide strong barriers of entry. Lastly, achievement of profitability through economies of scale threatens to allow NCNO to underprice new competitors. While management has outlined long-term 15% topline CAGR and operating margins of 35%, the main question revolved around how quickly NCNO will reach these margins, and for how long their strength will remain.

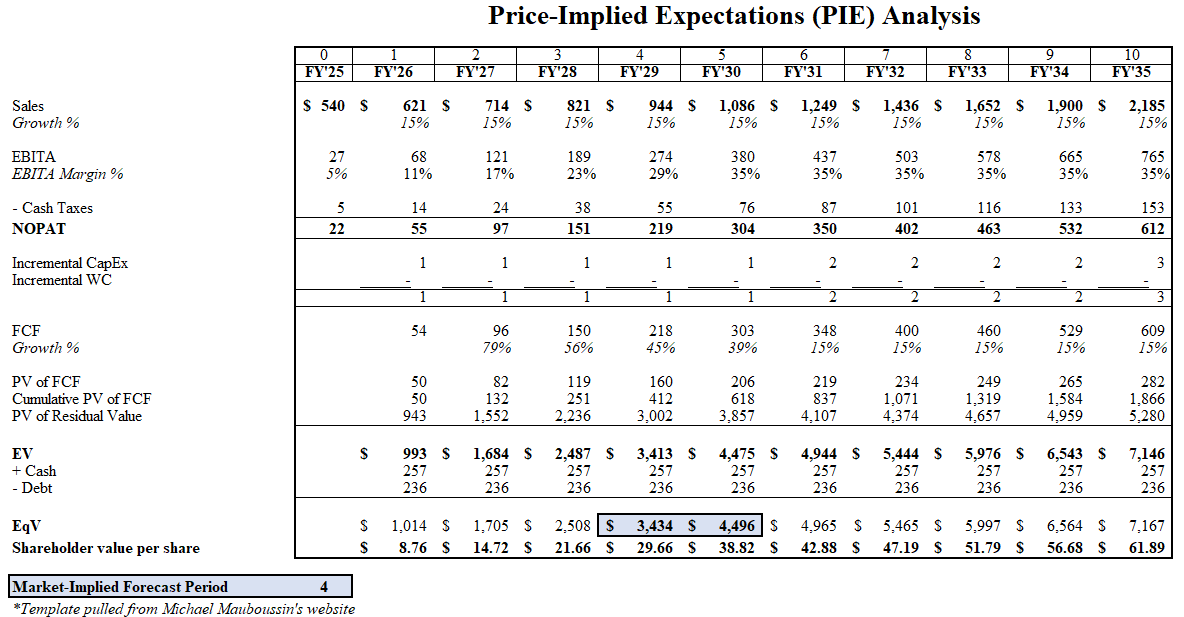

A quick forecast of NCNOs gradual gravitation towards 35% EBITA (~30% Operating margins + Amortization) margins paired with 15% revenue growth shows a market-implied advantage period of 5-6yrs (see chart and sensitivity table below); while I believe this time horizon understates NCNO’s strength, the returns are likely to be unimpressive in the following few years, and I am thus only slightly bullish on NCNO. This is a stock whose earnings will compound steadily at the back of one’s portfolio for years to come, but a ~40x NTM P/E makes a large purchase difficult to justify.