$CART Memo

Structurally Predisposed to Monopolize eGrocery

Instacart (NASDAQ:CART)

Synopsis:

As digital grocery delivery (“eGrocery”) enters its shakeout phase, the industry’s winner-takes-most dynamics should allow early superiority in large-baskets to create a fulcrum to industry-wide dominance. I believe eGrocery to be structurally predisposed towards third-party dominance, and CART’s existing density flywheel, superior customer experience and large-basket dominance gives it the right-to-win. This opportunity exists because of an overemphasis on the ad-driven narrative (which has thus failed to materialize), fear of competition from Amazon and an underappreciation of potential margins due to stale and inconsistent management guidance. By FY’28, I see a path to ~$90/sh, or +33% 3yr IRR.

Bio:

Maplebear Inc. (d.b.a. Instacart, “CART”) is a four-sided platform connecting consumers, shoppers, grocers, and advertisers to enable grocery delivery. While widely recognized for its marketplace, CART is a “grocery enablement partner,” providing the in-store picking, real-time inventory management, and last-mile delivery layers that sit atop a grocer’s operations. The company generates revenues through commissions charged to grocers, transaction take-rates and advertising take-rates. Commissions and transaction take-rates are combined intro “Transaction Revenue,” which encompasses ~72% of FY’25 rev.

Competitive Analysis

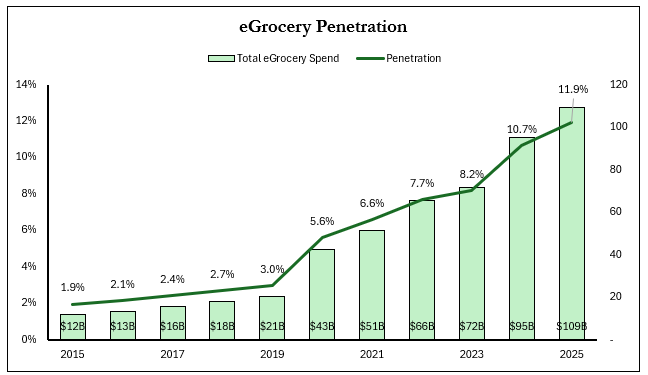

eGrocery has grown from ~3% of total grocery spend pre-Covid to ~12% in FY’25 (~$130B in Dec’25).1 While grocery stores have traditionally created habitual customers by combining proximity, convenience, and breadth and quality of selection, eGrocery is threatening to erode these advantages. In 2025, grocery spend began polarizing between retailers that emphasize price and those that emphasize quality.2 Grocers still control the relationship with consumers but the changing competitive landscape is forcing a strategic pivot to defend market share.

The central question in the still nascent eGrocery landscape is the viability of first-party (“1Ps) providers (Amazon, Walmart, DashMart) vs third-party layers (“3Ps”) (Instacart). While 1Ps could theoretically offer supply chain efficiencies and lower costs, the logistical difficulties and diseconomies of scale inherent in grocery delivery have forced a “hybrid” reliance on existing retail footprints. This hybrid approach suffers from the same structural disadvantages of 3P competitors without the latter’s agility.

Theses:

Why Does This Opportunity Exist?

Since CART’s Sep’23 IPO, the debate has shifted from the viability of the business model as grocers became non-exclusive, to the threat of competition, initially from other ride-share platforms, and finally to the slowing pace of growth, the monetization potential of ads and the potential threat from Amazon. Further, unremarkable growth has disillusioned many investors whop were hoping for a high-growth story, and the EBIT multiple has halved to ~11.5x.

The prevailing thesis – that CART can become a mini-Amazon that leverages marketplace to drive profit through ads – has stagnated as advertising take rates have hovered at 2.9% of GTV since IPO, below management’s 4-5% long-term guidance.3 However, the company’ internal focus seems to be have changed; mentions of advertising in company reports and transcripts fell -25% in FY’25 vs FY’23 and FY’24 and the unexpected departure of the previous CEO, who left in May’25 and was very ads-focused, opened the door to a new CEO cut his teeth on the retail side of both Instacart and Apple; his initial earning calls have explicitly focused on the importance of grocery partnerships. The other members of the C-Suite also predominantly have backgrounds in delivery logistics and retail, and the management website includes a Head of Connected Stores, but not a Head of Advertising.4 The narrative that CART is a mini-Amazon is outdated, and is a misunderstanding of CART’s internal focus and competitive strengths.

Thesis #1 – eGrocery is structurally predisposed to 3P dominance and fears of 1P competition are overexaggerated

Many are incorrectly categorizing eGrocery as a commodity where existing eCommerce capabilities will triumph; however, this overlooks the logistical complexity of perishables, the critical role of user experience and trust as key differentiators and 1P’s challenging unit economics. As eGrocery shakes-out, large-basket dominance should serve as a fulcrum allowing for increased market share gains throughout the spectrum of customers, and I believe CART is best positioned to reach a monopolistic position.5

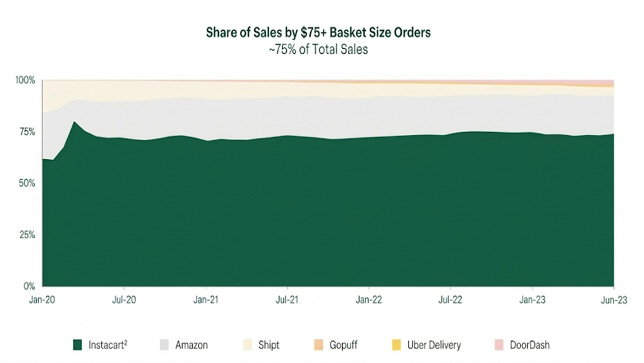

Importance of Large Baskets:

By dominating large-basket transactions, CART has created a flywheel that reinforces picking accuracy and that has shaped a differentiated shopper base. The eGrocery industry serves two types of consumers; those seeking small-AOV convenience orders that require competition on price and speed, and weekly shoppers whose large-AOV orders (>$75 average order value, 20+ items, 75% of total grocery spend) necessitate quality fulfillment and are less price-sensitive. Any platform that fails to offer a strong fresh-goods offering limits itself to small AOV convenience purchases and consumers who have to shop for fresh goods in person are likely to complete their entire weekly shop on-site.

From a unit-economics perspective, large-baskets are most attractive as shopper fees are relatively fixed and as AOV increases, per-order absolute profits increase proportionately. Moreover, there exists a distinct correlation between item count and complexity of order (due to more right-tailed items and wanning shopper focus) creating high barriers to entry. Consumers are less price-sensitive on large orders where the perceived “hassle” of a trip is highest, yet their expectations of picking quality (i.e. the accuracy of orders filled correctly, including the exact items, quantities, and quality) remain high, despite the compounded difficulty of fulfillment. A reliable large-basket solution creates sticky consumers.

CART’s lead in large-baskets was driven by early superiority in picking accuracy and consumer mental association. While competitors like DASH and UBER prioritize speed of delivery, CART’s shoppers spend >50% of their time in the store and must often communicate with consumers to clarify preferences and substitutions: this has attracted a differentiated shopper base that prefers shopping over driving. Today, roughly 70% of CART’s shoppers are women and ~50% are heads of households and as a shopper accrues experience, they move up the learning curve, becoming experts about the locations of products within stores, consumers’ replacement preferences, and the quality of product desired.

As a large-basket providers continue gaining disproportionate industry GTV, density and excess profits could be reinvested to provide a more cost-effective low-basket solution, creating a one-stop-shop for consumers’ grocery needs.

Logistical Advantage:

In logistics, the parallels drawn to eCommerce disregard the diseconomies of scale inherent in eGrocery distribution; orders are time-sensitive, products cannot be left unattended on the doorstep for extended periods of time (requiring a coordinated delivery time window), produce & meat are heterogeneous on the individual product-level, perishables are fragile & require temperature control, many items have a short shelf life, and the odd shapes of many SKUs preclude optimized packaging. Large fulfillment centers have limited effectiveness as their required automation and fixed costs necessitate extreme density, which is greatly complicated by these centers’ geographical isolation and high costs of transportation; Amazon’s fulfillment struggles drove their purchase of Whole Foods and Kroger recently paid $350M to shutter its automated centers. The need to deliver a basket within a certain time-window and high transportation costs results in batches of one-to-three orders and for a 3P deliverer, local proximity and a gig-workforce has largely decoupled an order’s speed and cost; conversely, 1Ps face a direct correlation between speed and cost, driven by the high expense of long-distance refrigerated transport. In 2h25, over half of industry-wide same day eGrocery purchases paid a premium for delivery within three hours and speed remains a key differentiator for consumers.

Further, by positioning itself as the go-to partner6 for the shift towards eGrocery and being the only pure-play eGrocery provider, CART has partnered with grocers and is shaping its strategy around the structure of the existing grocery industry. The first advantage of grocer integration is a more thorough view into on-shelf inventory, which increases accuracy, speed, and ultimately the platform’s convenience. To minimize substitutions, eGrocery’s platform must mirror a grocer’s on-shelf availability, which requires stringent on-shelf inventory management, a particularly thorny issue that mandates real-time surveillance of purchased items. This surveillance is best accomplished through a combination of technological integration into a grocer’s inventory management system and a fleet of shoppers who frequent aisles multiple times a day, essentially creating an in-person auditing team. High picking accuracy is a baseline necessity for consumers and even with CART’s integration, the average order still requires at least one replacement.

Convenience > Price

Another key misunderstanding about grocery delivery is an overemphasis on price; grocery shopping, either in-person or online, is not a commodity, but rather a process where convenience, broad selection, and trust are required. Order quality is a prerequisite for any eGrocery platform and can be disaggregated into picking accuracy (which is a function of on-shelf inventory visibility) and condition of product upon reception. Picking accuracy varies in difficulty across basket size, with large-basket orders tending to require more right-tailed unstandardized items and perishables. (CART’s orders average ~1 substitution). In addition, consumers have individualized preferences for their fresh goods (i.e. not all fresh goods are created equally, some consumers may desire a ripe avocado ready for immediate consumption while another may want an unripe one that can last until the end of the week). To perfect substitutions, a platform must thus be equipped to connect the consumer to the shopper, or, more likely, predict a viable alternative – without the substitution data set and shopper know-how accumulated within CART’s ecosystem, picking error rates are sure to be higher. While 1P distribution centers face a lower substitution hurdle due to greater inventory visibility, both WMT and AMZN are attempting to leverage existing store locations, exposing themselves to these same inventory management issues.

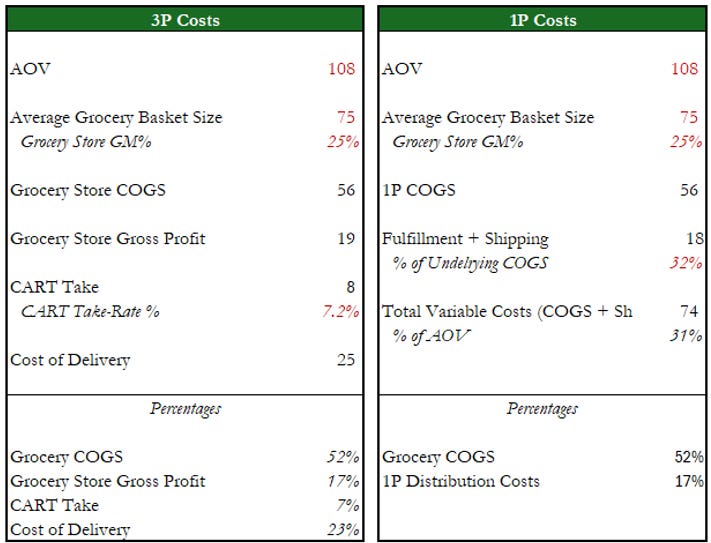

3P Remains Price Advantaged

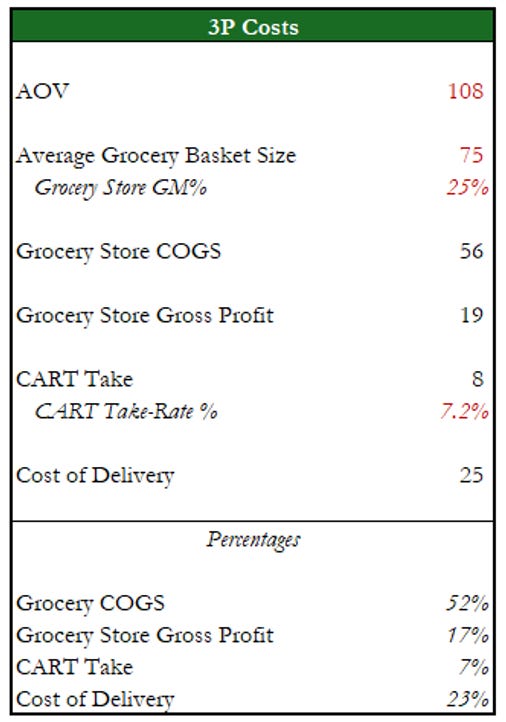

For a 3P, a density of orders decreases price while increasing speed and accuracy. An order’s AOV7 can be disaggregated into the underlying cost of grocery, the grocer’s mark-up, CART’s mark-up and shopper pay (which can be further disaggregated into tips and direct compensation). While grocery costs are outside of CART’s purview, grocer mark-ups are a function of the commissions charged by CART and the revenue uplift generated from being on CART’s platform; for the grocer, the fixed costs of operations and the platform are spread across a much larger pool of orders, enabling tightened mark-ups with a muted effect on gross margins.

Beyond reduced mark-ups, order density is a primary lever in reducing shopper earnings as concentrating multiple orders within the same location and time window enables shoppers to batch orders, fulfilling multiple orders in a single trip at lower pay/order, decreasing prices for consumers. Density also increases a shopper’s utilization and thus pay/hr, which CART has leveraged by decreasing minimum trip pay. I estimate non-tip shopper pay to constitute ~9% of average AOV, down from ~12% in 2Q’23. Increasing volumes also enable CART to flex its operating leverage as the majority of costs not captured in their take-rate are fixed; since FY’23,

Density also improves the quality of CART’s offering through a speedier product and improved picking accuracy. In FY’24, 50% of orders were fulfilled by shoppers within one mile from the store and a density of shoppers provides real-time data on shelf inventory availability, allowing CART to create its own inventory management solution, providing better data to consumers as to which items are available and at what price. Lastly, as more stores have reached a critical mass of shoppers, CART has created planograms – digital maps of a location’s layout that locate specific items – which further improves speed and accuracy.

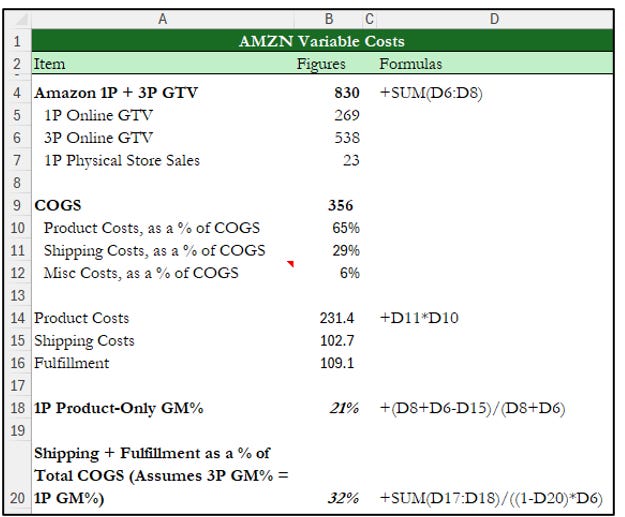

Theoretically, a 1P model could optimize the supply chain to circumvent grocer margins to enable lower prices, but this advantage has failed to materialize despite significant scale. The price of a grocery delivery can be split into three categories: the cost of the groceries, the cost of delivery, and the platform’s take rate. By disintermediating the grocer, AMZN could leverage its eCommerce playbook by subsidizing the cost of the order by eliminating retailer margins; the firm’s marketplace operates with a 21% gross margin and roughly breakeven operating margins (eCommerce alone barely makes a profit). If I assume the same cost structure will hold for eGrocery, gross margins could hover at ~31% if priced at CART’s AOV8 but directly translating eCommerce’s cost structure ignores the higher degree of variable costs from lower batch-rates, higher concentration of human-to-machine labor and the necessity for a sustained cold-chain throughout delivery.

These structural price hurdles are reflected in AMZN’s inability to offer consistently lower prices in its existing grocery offerings, despite ~$10B of GTV.9 Comparing a diversified set of grocery baskets across both value and upscale grocers on Instacart and Amazon Fresh and Whole Foods delivery, I found CART’s higher delivery prices to be offset by AMZN’s higher basket prices. Amazon Fresh was +18% more expensive than the mid-value grocer despite total delivery costs of $15 vs $21 and a delivery time of ~12hrs vs CART’s 1-2hrs; the biggest differentiator was the price of meat on Amazon Fresh, which was consistently almost twice as expensive as an in-person grocery store, illustrating the difficulties of transporting fresh goods. Similarly, Whole Foods delivery was +21% more expensive (+33% if I opted for a 1hr delivery window) and could be shipped in 3-5hrs compared to CART’s 1-2hrs. Anecdotally, the Amazon Fresh shopping experience was poor: many products were shown but actually unavailable, the platform kept switching between an eCommerce basket and an Amazon Fresh basket, and the delivery windows were inconsistent. Lastly, the prices of identical products were ~30% more expensive in Whole Foods delivery vs Amazon Fresh, providing another data point to the cost difficulties of operating a dense 1P distribution network. Whole Foods and Amazon Fresh used to offer free delivery for Prime members, but both had to introduce delivery fees to staunch unprofitability. Both conceptually and empirically, AMZN’s ability to undercut on price is limited, particularly for perishable goods.10 According to CART’s management, Amazon’s recent growth in grocery has been predominantly in baskets of <$50, reenforcing the view that AMZN is constrained to middle-aisle convenience items (Instacart’s S-1 cited Yipit, I believe this data point is likely from the same source).

Similarly, Walmart’s eCommerce segment (which includes more than just groceries and has a greater proportion of fixed costs) only recently became profitable, at ~$100B GTV. Of course, AMZN and WMT have the benefit of subsidizing their eGrocery operation through advertisements, circumventing CART’s necessity for profitability, but with this taken into account, 1P competitors will struggle to charge meaningfully less than CART.

Thesis #2: CART’s lethargic GTV growth is due to a behavioral bottleneck, not a market ceiling

Since IPO, investors have become disillusioned with what was hoped to be a high-growth company and the EBIT multiple has halved to today’s ~11.5x. However, the behavioral hurdles of eGrocery adoption are obfuscating a healthy runway of growth.

Grocery shopping is an entrenched weekly habit and, as with most innovations challenging the habitual status quo, incremental demand is a function of convincing unaware consumers of the viability of the new solution. Adoption is dependent on a mix of a strong retail experience, existing consumer recommendations (social proof), and trust.

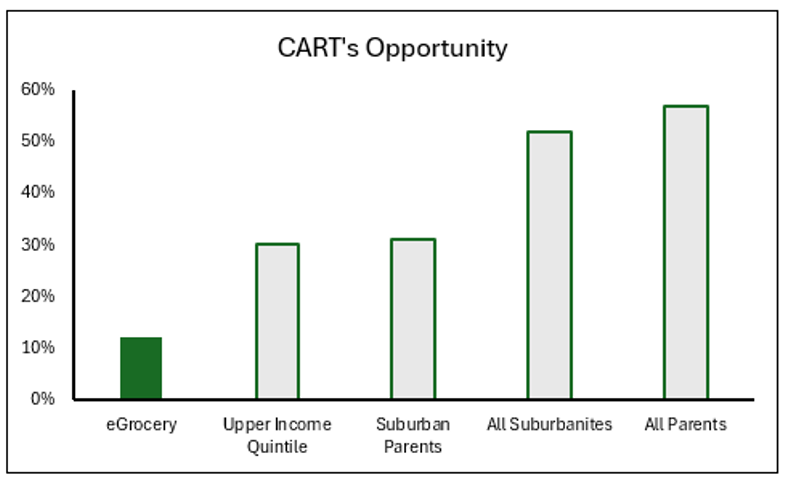

To quantify the scale of CART’s addressable market, eGrocery encompasses an estimated ~12% of grocery spend, a figure skewed upwards by the dominance of middle-aisle purchases. Perishable penetration is likely far lower. As for the potential consumer base, CART’s offering of convenience-for-a-premium is geared towards higher earning households for whom grocery is a chore (typically due to a combination of children and distance/suburbia); in the US, the uppermost quintile of grocery consumers encompass 30% of total spend (>50% for the two upper quintiles). Moreover, parents make up 57% of total grocery spend and a combined ~30% of the total is from suburban parents. As eGrocery’s awareness and credibility scales, eGrocery has the runway to a 2.5x-3x increase in penetration.11

Thesis #3: Consensus is underappreciating CART’s underlying earnings power

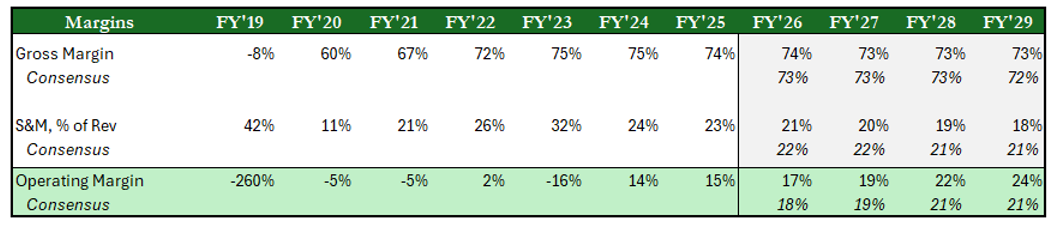

CART recognizes revenues on a take-rate basis, shifting most variable costs above the revenue line and while consensus forecasts cap operating margins at 21% (vs FY’25’s 15%), I believe marketing dynamics and inherent operating leverage should push margins higher.

As with most innovations challenging the habitual status quo, penetration is primarily limited by awareness and trust and adoption is a function of convincing unaware consumers of the viability of the new solution. An increasing user base will increases brand awareness and social proof and by aligning its incentives with its grocers, CART uses grocers as customer acquisition tools, allowing CART easy access to incremental consumers at the point of transaction rather than through expensive top-of-funnel advertising.

The underappreciation of CART’s potential margins is rooted in an overreliance on stale management guidance. Previous management guided to LT adjusted OpEx of 4.5-5% of GTV and the current CFO warned of slowing operating leverage, but current actions are inconsistent with these projections. Since FY’23, incremental operating margins have been ~50% and despite a strong FY’25, management opted against reinvesting into OpEx (which increased +2% YoY, adjusted for one-time FTC settlement), instead repurchasing $1.4B (~15% of the shares outstanding). The new CEO supposedly ranks share repurchases behind reinvestment and M&A, but recent actions suggest the business can scale organically without significant P&L reinvestment. To be blunt, I believe management is sandbagging the company’s true earnings power.12

Risks:

eGrocery spend could become increasingly fragmented, with CART’s utility narrowed to only perishables

If the convenience of receiving a single-basket erodes, customers could begin fragmenting spend across different platforms (i.e. CART only for perishables, AMZN only for middle-aisle). This fragmentation would decrease AOV, and fixed costs as a % of AOV would increase, resulting in a more expensive proposition for consumers. Expecting such purely profit-maximizing behavior at the cost of convenience from consumers is ambitious, but could be incented by drastic price cuts on non-perishables from competitors.

Incremental consumers could be more price-sensitive than expected

Higher-than-expected price sensitivity is equivalent to a misjudgment of current SAM, but overall TAM is constrained only by cost; if eGrocery becomes ubiquitously cheaper than in-person, TAM will inflect exponentially. CART’s SAM remains significantly under penetrated at the current price point, but adoption is contingent on the benefits of delivery outweighing the differences in cost. Interestingly, the financial parameters of CART’s existing consumer base roughly mirror those of the broader U.S. population and with growth recently inflecting, CART’s premium price point does not appear to be obstructing growth.

Agentic commerce could erode existing loyalties and diminish the importance of the user experience

Unlike human consumers, AI agents are agnostic to psychological or time friction and could erode loyalty to anything but price. This could create a more promiscuous shopping experience, but speed and quality of picking would remain crucial. Counterintuitively, this could be a boon for CART’s marketplace which could become the one-stop-shop for all grocery solutions, but shopping from multiple retailers would increase cost-per-order. Additionally, as agent-driven search has less product-loyalty, CPG ad-spend could inflect as shopping brands try to capture agents’ programmatic purchasing. Regardless, while AI cannot replace CART’s delivery or marketplace, a lack of human involvement in the purchase process could diminish CART’s superior and differentiated user experience.

Valuation

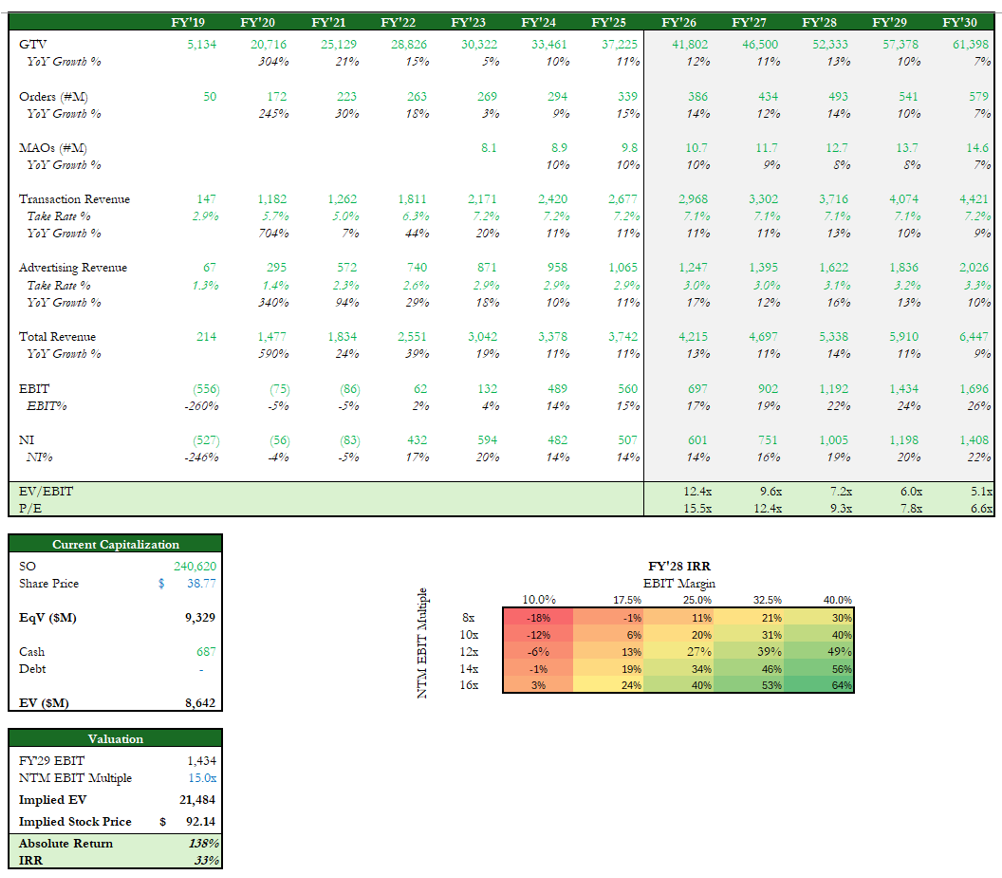

I value CART using a NTM EBIT multiple on FY’29 figures. My forecasts of continued +HSD MAU growth, stable take-rates, and increasing frequency as users increase platform trust result in +12% rev CAGR. I also forecast operating margin expansion to 24%. CART’s current NTM EBIT multiple of 11.5x thus implies a +23% 3yr IRR, but as the company’s competitive superiority becomes clear and it continues consistent growth, I expect expansion to a ~15x multiple (50% weight to the current valuation, 50% to UBER’s 18.5x). These inputs result in a +34% 3yr IRR, or +141% in absolute terms. My model is attached.

Appendix

Appendix A: Ad Segment Stagnation

There are two clear headwinds for ad-rev stagnation. First, as an intermediary, CART faces ad-spend cannibalization as limited budgets force advertisers to choose between in-person and online spend and as the majority of shopping remains in-person, advertising in-store is a necessary evil to guarantee shelf-space. Second, CART’s industry-leading conversion metrics are biased upwards by the intentional nature of consumers’ behavior on CART’s platform, and advertisers remain uncertain about the returns on ad-spend.

Appendix B: Amazon Fresh GTV:

Amazon disclosed an “Everyday Essentials” (groceries + middle-aisle consumables) GMV of $100B in FY’24, excluding in-person spend, and noted that these essentials grew at ~2x the rate of overall US eCommerce in FY’25. US eCommerce grew +10% in FY‘25, indicating a ~17.5% Essentials growth (lower than +20% since ex-Essentials eCommerce grew <10%); this implies $117.5B Essentials GMV in FY’25.

Total Grocery and Essentials FY’25 GMV is disclosed at ~$150B and in-person stores, which are almost entirely Whole Foods & in-person Fresh, was $23B. Thus, $150B (Total Grocery + Essentials GMV) - $23B (In-Person grocery GMV) - $117.5B (Essentials GMV) = ~$10B Fresh Groceries GMV.

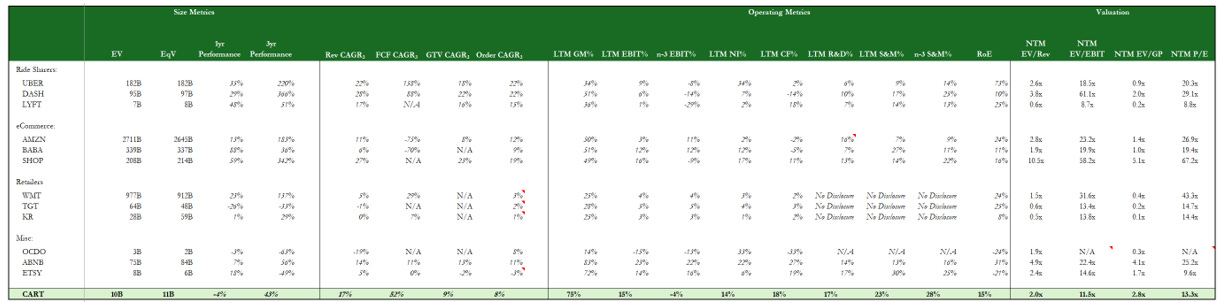

See Figure 1

Despite holding ~65% of in-person spend, supermarkets are struggling in eGrocery with a 27% share, lagging Walmart’s ~20% and 27% figures

Analysis of stagnation in Appendix A

CART’s proxy should be released in the next 1-2 weeks (Early April) – analyzing the respective salaries of top executives should paint a clearer picture of management’s priorities

See Figure 2

Examples of products include delivery and picking fulfillment, in-person smart shopping carts, order management platforms, catalog intelligence solutions, AI-powered shopping companions, integration into ChatGPT, and white-labeled retail media platforms

See Figure 3

See Figure 4

See calculations in Appendix B

See Figure 5

See Figure 6

See Figure 7 for my estimates vs consensus